Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

Notice

Third Avenue Management is aware of recent incidents involving unauthorized individuals and groups falsely claiming to represent Third Avenue Management and its affiliates through social media platforms, messaging applications, email, and fraudulent websites. In some cases, these bad actors have used the names, photographs, or identities of Third Avenue employees in an attempt to appear legitimate.

These individuals and websites are not affiliated with, sponsored by, or endorsed by Third Avenue Management.

Third Avenue Management does not solicit investments, provide investment recommendations, or request personal or financial information through social media platforms or messaging applications such as WhatsApp, Telegram, Signal, or similar services.If you receive a suspicious communication claiming to be from Third Avenue Management, we encourage you to verify its authenticity before responding or providing any personal or financial information. If you are unsure whether you are communicating with an authorized representative of Third Avenue, please contact us directly using the contact information available on our official website.

Third Avenue Management, its affiliates, directors, officers, employees, and agents are not responsible for communications, representations, or activities conducted by unauthorized third parties. If you believe you have been the target of an impersonation or investment scam, or that you or someone you know has been a victim of fraud, please contact your local law enforcement agency and report the incident to the appropriate authorities. In the United States, suspected internet fraud can also be reported to the Federal Bureau of Investigation's Internet Crime Complaint Center (IC3) at https://www.ic3.gov/.

These individuals and websites are not affiliated with, sponsored by, or endorsed by Third Avenue Management.

Third Avenue Management does not solicit investments, provide investment recommendations, or request personal or financial information through social media platforms or messaging applications such as WhatsApp, Telegram, Signal, or similar services.If you receive a suspicious communication claiming to be from Third Avenue Management, we encourage you to verify its authenticity before responding or providing any personal or financial information. If you are unsure whether you are communicating with an authorized representative of Third Avenue, please contact us directly using the contact information available on our official website.

Third Avenue Management, its affiliates, directors, officers, employees, and agents are not responsible for communications, representations, or activities conducted by unauthorized third parties. If you believe you have been the target of an impersonation or investment scam, or that you or someone you know has been a victim of fraud, please contact your local law enforcement agency and report the incident to the appropriate authorities. In the United States, suspected internet fraud can also be reported to the Federal Bureau of Investigation's Internet Crime Complaint Center (IC3) at https://www.ic3.gov/.

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

March 31, 2026

Real Estate Value Fund

Real Estate Value Fund Q126

Dear Fellow Shareholders,

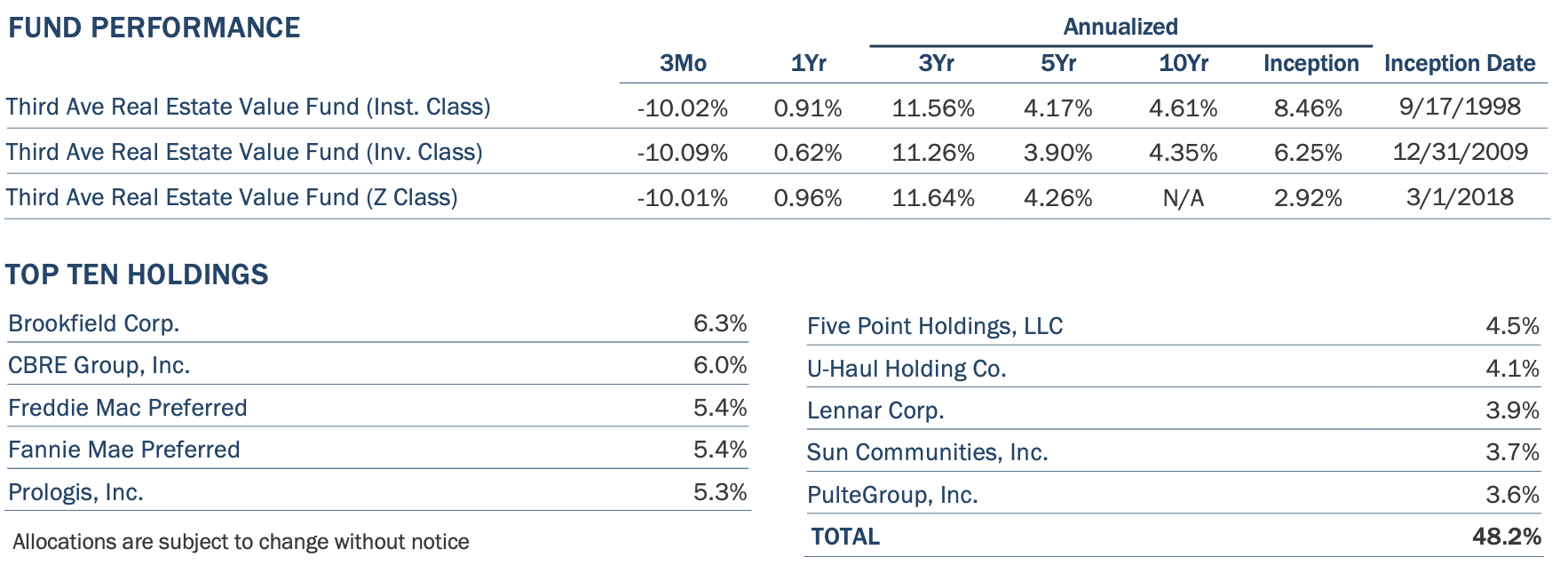

We are pleased to provide you with the Third Avenue Real Estate Value Fund’s (the “Fund”) report for the quarter ended March 31, 2026. For the most recent period, the Fund generated a return of -10.02% (after fees). In comparison, the Fund’s most-relevant benchmark, the MSCI ACWI IMI Core Real Estate Index¹, generated a return of +0.59% (before fees) over the same time-period.

The primary contributors to performance during the period included the Fund’s industrial real estate and logistics holdings (Prologis, WESCO International, and First Industrial) and certain Asian-based investments (CK Asset Holdings and Jardine Matheson Holdings). Notwithstanding, these gains were more than offset by detractors during the quarter, including the Fund’s investments in real estate services companies (CBRE Group, JLL, and Savills), residential-related businesses (Lennar Corp. and the preferred equity of Fannie Mae and Freddie Mac), and U.K.-based property companies (Big Yellow plc and Berkeley Group). Further insights into these enterprises, as well as Fund’s most recent additions (Brookdale Senior Living and Hang Lung Group) are included herein.

Recognizing that returns will vary over shorter periods of time, Fund Management continues to believe the Fund’s long-term results are the most relevant scorecard. To that end, the Third Avenue Real Estate Value Fund has generated an annualized return of +8.46% since its inception in 1998 (after fees). This performance indicates that an initial investment of $100,000 in the Fund would have a market value exceeding $900,000 at year-end (with distributions reinvested)—or more than the same $100,000 would be worth had it been placed into a passive mutual fund tracking the benchmark over the same time-period.

ACTIVITY

The Urban Land Institute and PwC collaborate each year to produce Emerging Trends in Real Estate, a widely followed report that synthesizes key insights across the property sector. The most recent edition included viewpoints from a wide range of senior professionals and proved to be rich in perspective, with the following themes standing out to Fund Management in particular:

- Durable interest in real estate from institutional investors, with target allocations remaining above 10.5%. Despite a slight decline, real estate remains a core pillar with some noting the asset class as “looking relatively attractive against other investments as a new cycle gathers momentum.”

- A further acceptance of property types that were once considered “niche”, including operational sectors such as self-storage, logistics, and senior living that are “now widely seen as capable of delivering higher, more stable yields amid compressing traditional returns”.

- A greater focus on investing in platforms versus individual assets, due to a more elevated cost of capital in the sector “shifting real estate returns towards operational performance and income growth rather than valuation gains”.

In combination, these concepts seem to support Third Avenue's long-held focus on well-established real estate enterprises. They also seem to offer a compelling backdrop for the Fund's recent investment in the common stock of Brookdale Senior Living ("Brookdale").

Founded in 1978, Brookdale is a leading owner and operator of senior housing properties with nearly 600 communities across the U.S. serving more than 50,000 residents. While the portfolio is vast, the company has a particular focus on assisted-living and memory-care properties, which sector specialists would point out as a more resilient segment with “needs based” demand and private-pay residents. Those same professionals would also likely perceive Brookdale as one of the premier operators in the assisted-living segment.

That said, the company has endured a difficult ten-year stretch. In fact, the Fund was previously invested in Brookdale but elected to move on after the previous management team made a somewhat hasty acquisition (i.e., Emeritus) at the same time the sector was facing elevated levels of supply. In combination with the headwinds the senior housing sector encountered amid the pandemic, Brookdale has generally been on the “defensive” in recent years shedding Emeritus locations, restructuring debt and associated leases, and attempting to stabilize its core portfolio.

While undoubtedly a challenging period, Fund Management believes the next five years will be transformative. To wit, Brookdale has solidified its financial position by returning to profitability and reducing its loan-to-value ratio below 40%, with the remaining debt largely comprised of non-recourse mortgage debt. The company has also improved its operational structure by adding a well-regarded CEO (with previous experience at industry peer Sunrise Living) and adopting a more decentralized framework. In addition, Brookdale has tremendous growth prospects with the opportunity to significantly increase its 82.1% occupancy rate alongside hugely supportive demand trends (i.e., the 80+ year-old demographic is expected to increase by 55% in the U.S. over the next decade).

As a result, Brookdale is positioned to close the performance gap with industry peers, in our view, as well as approach a 95.0% occupancy rate over time. Should such a path materialize, the company has the potential to generate more than $3.5 billion of annual revenues. By our estimates, a disproportionate share of that incremental cash flow would fall to the bottom line given the inherent operating leverage in senior housing (i.e., high fixed costs) and $2.0 billion of tax loss carry forwards.

Therefore, it would not be inconceivable for Brookdale to utilize retained earnings to further reduce its debt levels and reinstate an annual dividend. The company could also engage in additional “bolt on” acquisitions to expand its platform within core markets for the rapidly growing senior population. That said, such a scenario does not seem to be “priced in” with Brookdale trading at a discount to its owned real estate in our estimation—without factoring in any value for its operating platform, third party management business, or deferred tax assets.

Insights from the Emerging Trends in Real Estate report were not exclusive to the U.S., however. In fact, some of the more notable shifts internationally included (i) Asia Pacific’s “retail scene” offering “strong opportunities” and (ii) additional progress on the regulatory front further solidifying China’s real estate investment trust (“REIT”) market. Both of which seem constructive for the Fund’s recent investment in Hang Lung Group.

Founded in 1960, Hang Lung Group is a well-capitalized Hong Kong-based real estate enterprise that owns approximately 2.9 million square feet of highly leased retail and office properties in Hong Kong and Shanghai with a near net-cash position. Importantly, the company also owns a 65.1% interest in Hang Lung Properties, a separately listed real estate operating company with an additional 29 million square feet of retail centric properties in Hong Kong and Mainland China, as well as 10 million square feet of developments and residential projects available-for-sale.

In combination, Hang Lung Group is viewed to control one of the most productive (and valuable) retail-centric portfolios in the Asia Pacific region, with some of its iconic properties including Plaza 66 in Shanghai and the Fashion Walk in Causeway Bay. The path to establishing this platform has been far from easy though. As a matter of fact, Hang Lung Properties has spent the better part of three decades building out the core portfolio of its 11 market-dominant mixed-use locations, with more than $15 billion of “capex” in Hong Kong Dollars this decade alone. At one point, Hang Lung Properties even had to reduce its dividend, with Hang Lung Group electing to take shares instead of cash for further support.

Due to such strong sponsorship, Hang Lung Properties can now embark on a more operational focused strategy under Chair Adriel Chan at an opportune time. For instance, Hang Lung Properties is delivering its final ground-up mixed-use development this year (i.e., Westlake 66 in Hangzhou) at the same time prime retail locations seem to be benefitting from a rebound in retail sales, as well as a structural focus on further boosting consumption in the region. The supply-and-demand dynamics for the residential markets have also improved in Hong Kong and tier-1 Chinese cities more recently.

Therefore, it is not difficult to envision a path whereby Hang Lung Properties further improves its financial position beside residential sales, while reinstating a higher dividend alongside improved cash flows. Given the changes on the regulatory front, the company could also explore placing a portion of its highly recognized “66”-branded properties into a REIT vehicle to surface additional value over time.

Such actions would likely result in a material improvement to Hang Lung Properties’ cost of capital, with the stock currently trading at less than 40% of book value. That said, these developments would have a more significant impact for Hang Lung Group, in our view, when considering its stock trades at roughly 20% of book value, as well as more than 50% below the market value of its stake in Hang Lung Properties (without even factoring in the directly owned assets). Such a setup is referred to as a “double discount” at Third Avenue, and one that can be quite rewarding, in our experience.

Outside of these additions, Fund Management was active in further enhancing the portfolio positioning during the period. Of note, the Fund added to several holdings where the price-to-value gap broadened to historically wide levels amid recent volatility, including certain commercial-centric issuers (U-Haul Holdings and FirstService Corp.) and select international companies (Accor SA and Ingenia Communities). The Fund also trimmed back CK Asset Holdings, exited several positions following corporate activity (National Storage REIT, F&G Annuities, Rayonier, and Unite Group), and extended the Fund’s Hong Kong Dollar hedge.

POSITIONING

Following these changes, the Fund had 40.7% of its capital invested in U.S.-based companies focused on Residential Real Estate, including those involved with: Homebuilding (Lennar Corp., PulteGroup, D.R. Horton, and Champion Homes); Niche Rental Platforms (Sun Communities, AMH, and Brookdale Senior Living); Land and Timber (Five Point and Weyerhaeuser); and Mortgage and Title Insurance (Fannie Mae, Freddie Mac, and Fidelity National). In Fund Management’s view, each issuer has a well-established position in the residential value chain and is supported by a convergence of fundamental drivers, including: (i) historic demographic shifts, (ii) favorable supply-and-demand conditions for affordable product, and (iii) industry dynamics favoring scaled players.

An additional 30.2% of the Fund’s capital is invested in North American-based companies involved with Commercial Real Estate, including: Real Estate Services (CBRE Group, JLL, and FirstService); Asset Management (Brookfield Corp.); Industrial and Logistics (Prologis, First Industrial, and Wesco); and Self-Storage (U-Haul Holdings). In Fund Management’s opinion, these holdings represent platforms that would be very difficult to reassemble. They also comprise select pockets of commercial real estate that seemingly favor long-term investors with (i) structural demand drivers, (ii) limited maintenance “capex”, and (iii) prospects to “self-finance” value-enhancing initiatives.

The Fund also had 25.8% of its capital invested in International Real Estate companies. These businesses are largely focused on the same types of activities as outlined above, simply with leading platforms in their respective regions. At quarter-end, these included companies involved with: Commercial Real Estate (Big Yellow, CK Asset, Jardine Matheson, Segro, Wharf, and Hang Lung); Residential Real Estate (Berkeley Group and Ingenia Communities); and Real Estate Services (Savills and Accor). The holdings are also listed in developed markets where Fund Management believes there are (i) adequate disclosures and securities laws and (ii) ample opportunities for resource conversion and change of control transactions (i.e., the U.K., Australia, France, Hong Kong, and Singapore).

The remaining 3.3% of the Fund’s capital is in Cash, Debt & Options. These holdings include U.S.-Dollar based cash and equivalents, short-term U.S. Treasuries, and hedges relating to certain foreign currency exposures (Hong Kong Dollar and British Pound).

FUND COMMENTARY

During the quarter, the Third Avenue Real Estate Value Fund was named the Best Global Real Estate Fund Over Three Years and Five Years at the 2026 LSEG Lipper Funds Awards. As outlined in the Media Release, the Lipper Fund Awards have been synonymous with strong risk-adjusted performance for more than three decades, and the 2026 Awards mark the eighth time the team has been recognized in the Best Global Real Estate Fund category.

In Fund Management’s view, this recognition is largely attributable to the distinctive positioning of Third Avenue’s Real Estate Value strategy, as well as the team’s commitment to continuous improvement. It also reinforces our long-held view that an actively managed fund, backed by a sound strategy, robust process, and aligned portfolio management team, holds strong prospects to outperform benchmark-oriented strategies over time.

However, one of the primary drawbacks of a strategy with high active share (i.e., minimal overlap with its benchmark) is inevitable periods of underperformance. This is especially the case for funds that concentrate their capital around select holdings and hold for longer periods of time (i.e., low turnover strategies). The Real Estate Value Fund experienced precisely this dynamic during the quarter, with the divergence primarily stemming from three pockets within the portfolio, including:

- Real Estate Services: The Fund has held positions in leading real estate services companies for several years (CBRE, JLL, and Savills) as they are not only well-capitalized but have reshaped their business models with significant recurring revenues. At the same time, these companies have taken market share in the core transactions and leasing segments. The real estate services companies held in the Fund have also reported solid results more recently, increasing earnings per share by more than 25% over the past year, on average. That said, their stock prices declined markedly during the quarter amid "AI fears". While Fund Management recognizes potential changes, it is our view that these companies are “AI beneficiaries” as their complex transactional work is less prone to automation and certain processes can be streamlined for efficiency. In addition, each enterprise has an expanding data center business, as well as modest implied value for its transactional segments (i.e., less than 10 times operating profits).

- Residential-Related Businesses: The U.S. residential markets exhibited signs of improving fundamentals to start the year before interest rate (and mortgage rate) volatility transpired. In Fund Management’s view, such a setback is likely to be temporary given the long-term fundamental setup, along with well-capitalized Fund holdings Fannie Mae and Freddie Mac stepping in to foster additional liquidity in the mortgage-backed security market to enhance affordability. That said, certain company specific items impacted performance, including at Lennar Corp.—a leading U.S. homebuilder that has pivoted to be more “land light” and “production focused” in recent years. During the quarter, the company’s stock price declined as Lennar continued to offer incentives (i.e., mortgage rate buydowns) to meet its annual delivery pace of 85,000 homes, which has pressured its margins while overshadowing the improvements in its inventory turns and returns on capital. As a result, Lennar’s B shares now trade below book value and less than 6 times peak earnings, which seem attainable again should incentive levels normalize over time, in our view.

- U.K.-Based Holdings: The U.K. remains a compelling property market in Fund Management’s perspective, with favorable supply-demand dynamics, strong property laws and deep capital markets. However, recent energy-driven inflation and higher capital costs have weighed on U.K. property stocks. Fund Management believes that pressure is likely to subside over time and may even accelerate the domestic sourcing of critical resources. Further, the Fund's holdings seem positioned to navigate these "stagflation light" conditions with strong balance sheets and prospects to increase cash flows across structurally supported niches, not to mention discounted valuations. For instance, Big Yellow (the largest owner of self-storage facilities in the U.K.) was a detractor in the period with its near-term results likely impacted by higher utility costs. That said, the long-term opportunity seems significant as Big Yellow’s stock price implies an 8.5% “cap rate” for its hard-to-replicate portfolio, without even factoring in the lease-up potential with 20% of the portfolio vacant.

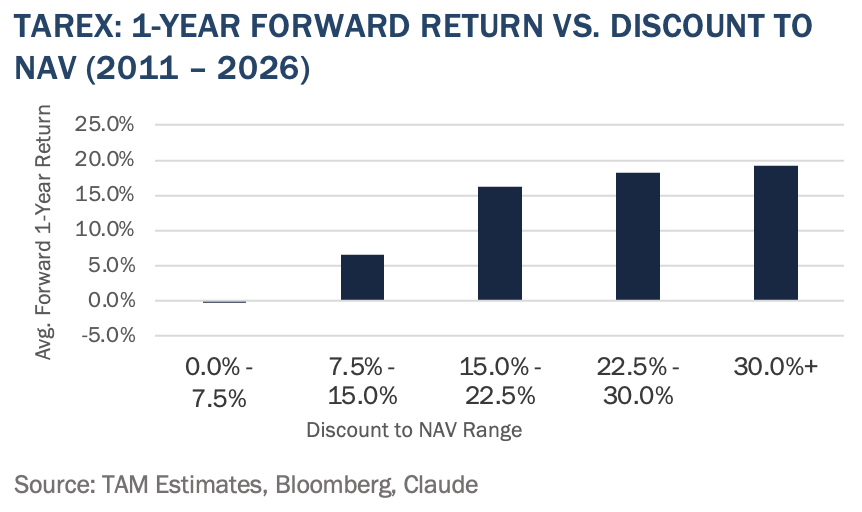

Considering this backdrop, the divergence in performance for each one of these allocations this quarter seems to be temporary in nature, in Fund Management’s opinion. Furthermore, the price-to-value proposition for those positions, and the Fund’s holdings more generally, is now approaching historically attractive levels as a result. For better perspective, the Third Avenue Real Estate Value Fund’s holdings were trading at an average discount of nearly 30% at quarter-end in the aggregate—a level that has only been reached three other times in the past 15 years (i.e., 2011, 2020, and 2022).

Similar to those other moments, Fund Management has implemented a familiar playbook. That is to say that amid the most recent bout of market volatility, the Fund has (i) utilized excess cash to increase existing positions where the discount to a conservative estimate of its corporate net-worth has widened materially, (ii) recycled capital by exiting certain holdings in order to redeploy the proceeds into select issuers with even superior long-term return prospects, and (iii) personally added capital to the Fund.

While each one of those prior instances undoubtedly had its own specific set of circumstances, they ultimately did share a common theme: serving to be among the most rewarding times to be invested in the Fund prospectively. In fact, there has historically been a strong correlation between prospective returns for the Fund and the underlying valuations for its holdings over the past 15 years, as illustrated in the following chart.

Only time will tell whether the Fund’s existing price-to-value proposition translates to similar performance in this instance. There is one near certainty though: the Third Avenue Real Estate Value Fund will remain invested in well-capitalized and strategic real estate enterprises trading at modest valuations over that period—whether they are significant parts of the benchmark or not.

We thank you for your continued support and look forward to writing to you again next quarter. In the meantime, please don’t hesitate to contact us with any questions or comments at realestate@thirdave.com.

Sincerely,

The Third Avenue Real Estate Value Team

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of March 31, 2026 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: April 15, 2026

1 The MSCI ACWI IMI Core Real Estate Index is a free float-adjusted market capitalization index that consists of large, mid and small-cap stocks across 23 Developed Markets (DM) and 24 Emerging Markets (EM) countries engaged in the ownership, development, and management of specific core property type real estate. The index excludes companies, such as real estate services and real estate financing companies, that do not own properties. Results for the index are inclusive of dividends and net of foreign withholding taxes.

For the Third Avenue Glossary please visit here.

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the Fund’s Institutional, Investor and Z share classes is 1.18%, 1.43% and 1.11%, respectively, as of March 1, 2026.

Distributions and yields are subject to change and are not guaranteed.

Risks that could negatively impact returns include: overbuilding and increased competition, increases in property taxes and operating expenses, lack of financing, vacancies, environmental contamination and its related clean-up, changes in interest rates, casualty or condemnation losses, and variations in rental income.

The Morningstar Rating™ for funds, or “star rating,” is calculated for mutual funds, variable annuity and variable life subaccounts, exchange-traded funds, closed-end funds, and separate accounts) with at least a three-year history. Exchange-traded funds and open-ended mutual funds are considered a single population for comparative purposes. It is calculated based on a Morningstar Risk-Adjusted Return measure that accounts for variation in a managed product’s monthly excess performance, placing more emphasis on downward variations and rewarding consistent performance. The top 10% of products in each product category receive 5 stars, the next 22.5% receive 4 stars, the next 35% receive 3 stars, the next 22.5% receive 2 stars, and the bottom 10% receive 1 star. The Overall Morningstar Rating for a managed product is derived from a weighted average of the performance figures associated with its three-, five-, and 10-year (if applicable) Morningstar Rating metrics. The weights are: 100% three-year rating for 36-59 months of total returns, 60% five-year rating/40% three-year rating for 60-119 months of total returns, and 50% 10-year rating/30% five-year rating/20% three-year rating for 120 or more months of total returns. While the 10-year overall star rating formula seems to give the most weight to the 10-year period, the most recent three-year period has the greatest impact because it is included in all three rating periods. Morningstar Rating is for the Institutional share class only; other classes may have different performance characteristics.

©2026 Morningstar, Inc. All Rights Reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete or timely. Neither Morningstar, nor content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

The fund's investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting www.thirdave.com. Read it carefully before investing.

Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through '40Act mutual funds and customized accounts. If you would like further information, please contact a Relationship Manager at:

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.