Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

June 30, 2025

Value Fund

Value Fund Q225

Dear Fellow Shareholders,

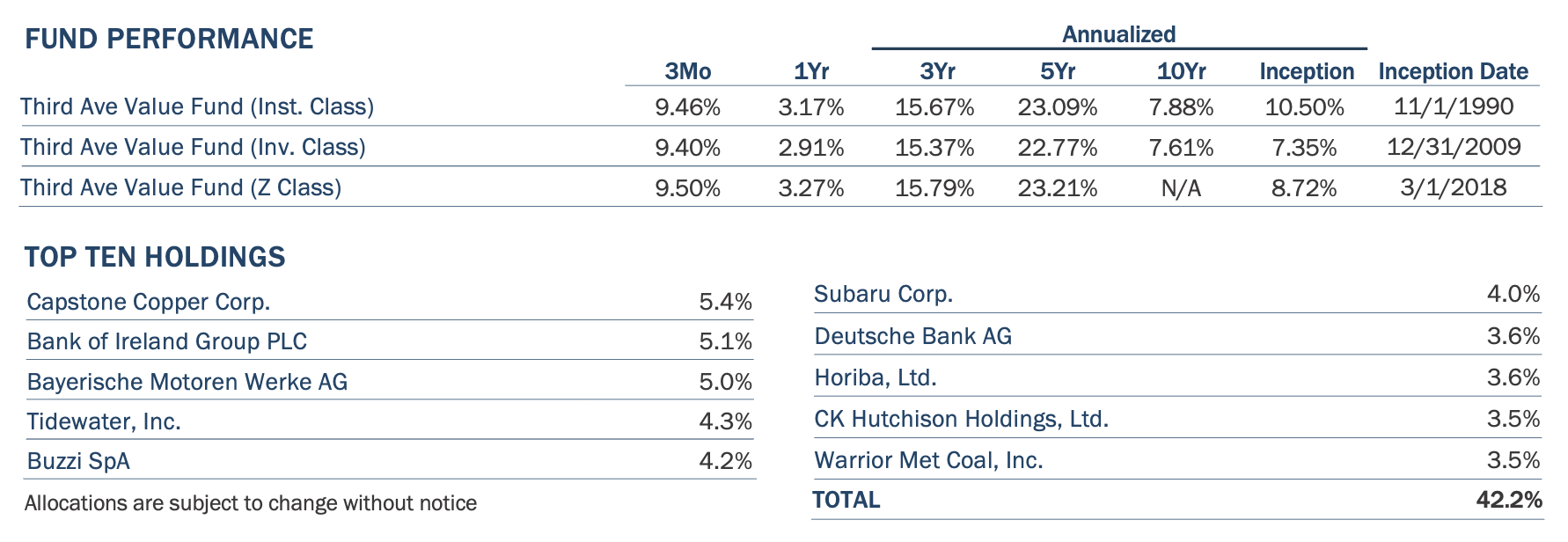

For the three months ended June 30, 2025, the Third Avenue Value Fund (the “Fund”) returned 9.46%, as compared to the MSCI World Index1, which returned 11.63%, and the MSCI World Value Index2, which returned 5.62%. For the year-to-date period, the Fund returned 12.69%, compared to the MSCI World Index and the MSCI World Value Index, which returned 9.75% and 10.91%, respectively. As of quarter end, annualized Fund performance for the trailing three-year and five-year periods was 15.67% and 23.09%, respectively.

PERFORMANCE REVIEW

During the quarter, smaller-capitalization companies staged something of a recovery. For example, the MSCI World Small-Cap Index3 produced a return of 11.73% during the quarter, slightly outperforming many major global large-cap indices. Curiously though, that phenomenon was mostly an international one in the sense that U.S. small-cap stocks continued to markedly underperform U.S. large-cap stocks during the quarter. For example, the S&P 5004 Index returned 10.94% during the quarter, while the S&P SmallCap 6005 Index returned 4.90%, widening an already significant gap on a year-to-date basis.

For the Fund specifically, strong performance during the quarter was driven by investments such as U.K. low-cost airline, easyJet, European banks, Bank of Ireland, Deutsche Bank and Close Brothers, two copper mining companies, Lundin Mining and Capstone Copper, and German auto manufacturer, BMW. Several other positions made important contributions as well. On the other side of the ledger, digital media company, S4 Capital, provided a drag on portfolio performance. Additionally, Canadian lumber company, Interfor, Japanese cement company, Taiheiyo Cement, U.S. insurance company, Old Republic, and Japanese auto company, Subaru, each provided very modest negative contributions to Fund performance.

FOOD FOR ASSET ALLOCATOR THOUGHT

During the quarter, I was honored to participate in two highly regarded annual investment conferences, both of which gather decidedly value-oriented groups of attendees. Given my presumption that attendees would have a penchant for value-oriented, price-conscious forms of investing, I was somewhat taken aback during my participation in one value investing panel by resistance to the idea that U.S. large-cap stocks may present an unusual amount of risk at present. One question posed to our panel was whether U.S. large-cap companies, the mega-cap variety in particular, deserved to be accorded such large valuation premiums because the companies and their business models are of uniquely high quality, a question somewhat intertwined with the notion of American exceptionalism.

After the panel, I enjoyed several conversations with sophisticated investors who also offered further comments in support of the small set of U.S. mega-cap companies as attractive investment propositions. One central point put forward was that, among the U.S. mega-cap companies, there are extraordinarily attractive business models that have never existed before and the nature of which offer “winner take all” opportunities. To my recollection, the relationships of security prices to the economics of the businesses were not part of the supporting arguments.

Still, these conversations have given rise to more reflection on my part and compelled me to share a few additional thoughts on the subject. I have lived and invested through periods in which large equity market declines have inflicted significant financial harm on a great many investors. As we write today, U.S. household allocations to equities have rarely, if ever, been higher in more than 70 years of record keeping by the U.S. Federal Reserve. Even for highly sophisticated professional investors building diversified portfolios, it is conventional to use a global equity benchmark as a frame of reference. Yet, global equity benchmarks have also rarely, if ever, been more heavily weighted to U.S. large-cap stocks. This phenomenon of record portfolio weightings to U.S. large-caps is occurring at precisely the same time that U.S. large-cap equity indices have themselves rarely been more concentrated into a handful of very large companies. In short, huge exposures have accumulated in ostensibly very expensive stocks as a result of the past share price performance of a small number of very large companies. This is a natural but undesirable outcome of the way portfolios evolve over time if they are not rebalanced.

“In fact, the world of commerce (as opposed to the world of investment) generally rewards following the trend…In the Darwinian world of business, success breeds success. In the world of investments, failure sows the seeds of future success. The attractively priced, out-of-favor strategy provides much better prospective returns than the highly valued, of-the-moment alternative.”

David Swensen – Pioneering Portfolio Management, An Unconventional Approach to Institutional Investment

A few years back, our team wrote a whitepaper analyzing the question of whether low interest rates justified U.S. growth stock outperformance. This was a very common rationalization at the time but was not the first narrative used to rationalize the prevailing high prices of U.S. mega-cap growth stocks. When rationalizations shift over time - from disruption and innovation to hyper-low interest rates to unique quality and American exceptionalism – all to justify the same phenomenon, one might rightly grow increasingly skeptical. Rather than shape-shifting rationalizations, maybe a more consistent contributing cause of increasing valuations has been a self-reinforcing cycle of attractive fundamental performance, leading to both domestic and foreign investment flows, momentum, and rising valuations, producing a positive feedback loop encouraging more of the same. Persistent flows into passive strategies, persistent strength of the U.S. dollar, very significant outperformance of the market cap weighted S&P 500 Index relative to the equal weighted version of itself, and rapidly rising foreign ownership of U.S. financial assets, all coinciding with one another in recent years, certainly support that suspicion. Meanwhile, during the first half of 2025, the U.S. dollar experienced its worst first semester depreciation in roughly half a century and it occurred in concert with material underperformance by U.S. large-cap stocks relative to the non-U.S. stocks. This is again consistent with the thesis that foreign capital inflows had been playing a role in propelling the valuations of U.S. large-cap stocks.

Meanwhile, there are many lenses through which one can analyze index valuation. For those who study such things professionally, such as Nobel laureate Robert Shiller, the Cyclically Adjusted Price to Earnings (CAPE) ratio of an index, such as the S&P 500 Index, has generally proven to be an excellent predictor of returns over longer periods, meaning the next ten years. It is, however, an admittedly poor predictor of near-term returns. In statistical terms, during the last century the CAPE ratio has shown a very strong negative correlation to returns over the next ten years. In other words, the higher the valuation, as measured by the CAPE ratio, the worse the prospective long-term returns. With the current CAPE ratio of the S&P 500 Index reading in extremely rarified air, it would be very unsurprising if longer-term returns for U.S. large-cap stocks were quite poor from this starting point and rationalizations of U.S. large-cap index valuations quickly paint us into a corner of having to make statements uncomfortably similar to “this time is different,” one of the most sinful phrases in investing.

The notion that a business can be of such exceptional quality and its prospects so bright and predictable that it does not matter what one pays for a share of ownership has certainly been proffered before. The idea harkens directly back to the 1960s and 1970s era of the “Nifty Fifty”. Companies like Polaroid, Xerox, and IBM became the face of that era and were perceived as the quintessential “one-decision stocks”, which were only to be purchased and never sold. This was also an era in which reputational and career risk from not owning certain incredibly popular, high performing stocks rose to the fore for professional money managers. That concept has never been more prevalent than it is today, a period which has aptly been described as a bear market in diversification and proven to be a cataclysm for active equity management broadly.

Moreover, the idea that the quality of a company can be so special that conventional notions of security valuation are not relevant implicitly suggests that a specific degree of quality is intrinsic to a business or a company. That belies what is, in our view, a much more real-world view that the quality of a business is not an immutable trait but is constantly evolving over time. The fortunes of all businesses, the environment in which they operate, the regulatory environments to which they are subjected, geopolitical headwinds and tailwinds, executive changes and competitive threats, and, in turn, the company’s operating results evolve over time.

Some businesses improve, while others deteriorate. Just ask the folks from Kodak, Intel, GE, etc. Apple, one America’s greatest corporate success stories, was directionless and within weeks of insolvency in the mid-1990s, only to later become unimaginably successful. Today its entire hardware business is inextricably dependent upon a one-of-a-kind Chinese supply-chain and, by extension, the Chinese government. Is it so difficult to imagine how life could become materially more challenging for Apple? Those who are willing to internalize the realities of business and investment uncertainty often develop a strong compulsion to invest in businesses at prices reflective of uncertainty.

Lastly, we have implicitly been speaking about the relationship between business quality and valuation as though there is a direct linkage. A better representation is that a business has some fundamental economic strengths and weaknesses and the observably fickle public perception of those prospects, in the eyes of equity market participants, is what is represented in price and valuation. Perception appears even less immutable than actual underlying business quality.

Imagine that equity market participants wake up one day and focus on the fact that the S&P 500 Index has a top ten position in a trillion dollar market cap auto manufacturer, that I) is being competitively decimated in China, the world’s largest auto market, II) has, during the last five years, lost roughly one third of its market share in the U.S, the world’s second largest auto market, III) is subject to a quasi-boycott and precipitous volume declines in Europe, the world’s third largest auto market, IV) appears likely to imminently lose very large government-provided purchase subsidies to its U.S. customers and also lose its ability to sell billions of dollars of U.S. carbon credits, which comprise a substantial portion of its profit, and V) would, by our math, be subject to a valuation decline well in excess of 90% were it to be valued like some of the very best auto manufacturers in the world? Those fundamental quality considerations are in plain view today. What if perceptions changed and investors decided they no longer thought it advisable to bet nearly one trillion dollars of market capitalization on non-auto activities that do not yet exist as businesses? If our message is clearly understood, this will not be read as condemnation of a single company but as a statement that the price one pays for an investment has a profound relationship to the investment risk being incurred. The same company can be an extremely attractive and safe investment at one price and an incredibly risky and unattractive investment at another price. And because the price one pays for an investment may be the single most important determinant of the amount of investment risk being incurred an abandonment of price-consciousness, in reaction to one’s admiration of a business, is synonymous with an abandonment of risk-consciousness.

Meanwhile, for asset allocators, one needs to work a little harder than usual these days to find genuine diversification from historically expensive U.S. mega-cap stocks. Paradoxically, while active, price-conscious, fundamental strategies may be near the nadir of their popularity today, that may be precisely the time at which they are most valuable and needed for their diversification and risk-control benefits. It should also be said that some active fundamental strategies have produced very attractive long-term absolute and relative returns as well. The long record of paying any price to own companies widely perceived as exceptional and defining risk as the danger of not owning certain stocks has been very unkind. Maybe this time is different but that appears to be an extremely high risk, low probability bet.

GRIST FOR THE MILL

Whereas many investors are often acutely focused on their perception of quality and business outlook, value investing is an inherently price-conscious approach which tends to emphasize opportunities in which securities can be purchased at meaningful discounts to estimates of business value. In the context of such an approach, and in contrast to the skepticism articulated above, we contend that there are some very appealing value opportunities within global equity markets today.

During the last six calendar quarters, the Fund has initiated six new positions, three of which are listed in the U.K. and three of which are listed in Japan. Aside from both markets experiencing a considerable amount of investor pessimism and neglect, the two sets of investment opportunities share little in common. We discuss our latest U.K. investment in detail below and would like to share some detail and opinion regarding the large and growing Japanese weight within the Fund today.

As a percentage of the Fund, Japan represented approximately 16% at quarter end. These holdings, in order of weight, are Subaru Corporation, HORIBA Ltd., Taiheiyo Cement Corporation, Paltac Corporation, and JEOL Ltd. In our view, the businesses within this portion of the portfolio are of very high quality, are extremely well-financed, and seem peculiarly inexpensive. While investing in Japan does require navigating some idiosyncrasies, there seems to be a large dissonance between the distressed pricing of various businesses and their excellent operational and financial health. This portion of the Fund is one reason for our optimism about the Fund’s prospects for future performance, among several others. We think we have good grist for the mill.

When looking at the weighted average valuation6 of the Fund’s Japanese holdings, the group of companies was valued at 1.1x tangible book value at quarter end, while having grown tangible book value per share by greater than 15% annually over the last five years through March 2025, inclusive of dividends. The companies are collectively valued at a very modest multiple of 6.5x enterprise value to trailing EBIT (earnings before interest and taxes) and have collectively grown EBIT by more than 15% annually over the same trailing five-year period. Meanwhile, earnings per share for the group have grown by more than 14% per year over the last five years, a particularly impressive result for companies that are collectively valued at only 9.6x earnings today. The collective profitability and financial strength of this group of companies has supported a 3.2% trailing dividend yield, a rather high figure for Japanese companies, and material share buybacks by four of the five companies in recent years. If one were to look at business performance on a cash-adjusted basis, using a return on invested capital figure, for example, the business performance looks downright exceptional for a few of our Japanese holdings.

Furthermore, the five Japanese company investments we have assembled to date comprise a wide range of industries, end market exposures, currency exposures, and risk factors. In other words, while our approach is to seek distressed valuations attached to companies that are not distressed, it is sometimes the case that pockets of opportunity can lead to concentrations of fundamental risk when those valuations arise in a single industry or as a result of common macroeconomic factors. In this case, however, we have purchased an auto company with the large majority of its business in the U.S., a cement company with highly localized businesses in the U.S. and Japan, two companies that make critical pieces of equipment used in global semiconductor manufacturing and scientific testing, and Japan’s largest consumer products distribution company. There are companies in the group with some export and currency exposure risk, such as Subaru, while others have virtually none. For example, Paltac, the largest company within the oligopoly that controls the distribution of Japanese consumer products to drug stores and convenience stores, is a highly domestic Japanese business serving primarily domestic producers and consumers of a huge range of consumer products through world-class distribution facilities.

Furthermore, these five companies are very well-financed individually and collectively. Collectively their net cash and investments represent more than a third of their market cap and EBITDA (earnings before interest, tax, depreciation, and amortization) covers interest expense by more than 1,000x. The range of financial positions is bookended by Subaru on one end, a company with net cash and investments rivalling its entire market capitalization, and by Taiheiyo Cement on the other. Taiheiyo, the Fund’s only Japanese portfolio holding without a net cash position, has net debt totaling roughly 2.4x its last twelve months EBITDA. Its financial position is even stronger when considering its holdings in liquid investment securities, which is a characteristic it shares with our other Japanese investments. Interestingly, the majority of Taiheiyo’s profit and business value derives from its large U.S. cement business, an industry in which many companies carry net debt similar to Taiheiyo’s or higher given the exceptional historical operating performance and resilience of that business.

However, whereas decent U.S. cement businesses are often valued at greater than 10x EBITDA in public markets and in takeover transactions, Taiheiyo is today valued at roughly 5.6x EBITDA. As an interesting parallel to the earlier section of this letter, in recent periods there has been a wave of spin-offs of U.S. cement assets and changes of listing to the U.S. by global cement companies, many of which have large underlying U.S. businesses. Those companies are attracted to the opportunity to avail themselves of far higher valuations assigned to U.S.-listed assets, even though the underlying businesses portfolios have not changed at all. This type of valuation arbitrage activity remains a potential opportunity for cement company Taiheiyo (as well as similarly situated portfolio holding Buzzi Spa, a cement company listed in Italy). However, across a wider spectrum of Japanese businesses, the scope of the potential to create shareholder value by highlighting underlying business value through spin-offs, divestitures, relisting, and other resource conversion activity remains difficult to overstate.

With regard to the broader Japanese opportunity, we have been encouraged by the growing drumbeat of pressure to improve corporate governance in Japan. While foreigners continue to pursue activist campaigns as they have for decades, what is fundamentally new about this era is that it was born from within Japan. Organizations at the highest levels of the Japanese business world, including the Tokyo Stock Exchange (“TSE”), the Bank of Japan(“BoJ”), Japan’s Government Pension Investment Fund (“GPIF”) and the influential Ministry of Economy, Trade and Industry (“METI”) have all engaged in a concerted effort to broadly improve corporate governance standards. The TSE for example has led an effort to benchmark corporate results in important areas related to returns on capital, going so far as to name and shame boards of directors and executive teams it perceives as not making a concerted effort. Considerable pressure has mounted to reduce excessive capital retention and an endless web of Japanese cross-shareholdings among companies. There has also been a major push to reduce the prevalence of publicly listed, but fully controlled, subsidiary companies, often referred to as parent-child companies in Japan. The high-level governmental and financial market support has incubated a growing domestic Japanese activist community, which has grown increasingly large and active over the last few years. The number of activist shareholder proposals at Japanese annual shareholder meetings has exploded. This is all very encouraging, and it would be impossible to say that some progress has not been made.

Continued progress could certainly impact each of our companies in important ways. Paltac happens to be one of those controlled subsidiaries mentioned above, for example. Several of our companies have more net cash and investments than we view as reasonable. A domestic activist investor has taken a position towards the top of the shareholder registry at one Fund holding. Further, the combination of low valuations and overcapitalized balance sheets gives rise to a huge opportunity to create shareholder value through share buyback activity, which has grown in frequency but could be pursued far more aggressively.

Pointedly, there can be little debate that Subaru is the most overcapitalized Japanese company held by the Fund. For comparative purposes, it is important to understand that numerous other auto companies, including Fund holdings BMW and Mercedes-Benz as well as Subaru’s largest shareholder Toyota Motor, have large captive financial services businesses, which require them to access capital markets recurrently. For that reason, credit ratings are an important consideration and holding significant net cash positions is a prerequisite for those automakers. However, BMW and Mercedes-Benz are also overcapitalized well beyond those required levels. For that reason, both companies have recently communicated to investors that they intend to distribute approximately 100% of the free cash flow generated by their auto-making businesses, given a lack of need to retain additional capital. Subaru has no such financial services business and is not in need of regular access to capital, making its enormous financial position and shareholder return policies even more out of place.

In fairness, a little bit of historical perspective and appreciation of a few business idiosyncrasies are important here. While we would describe Subaru as a financially conservative company, it does not appear to us to be one of the many Japanese companies that have carried on for decades in a grossly overcapitalized state. Prior to COVID, the company began to accumulate significant capital in its planning for a potentially very expensive battery electric vehicle (“BEV”) transition. Then, at least initially, the uncertainty of the pandemic put all global auto companies in a more conservative posture. It was not anticipated by Subaru or others that a rapid recovery would ensue and an unusually profitable period for auto manufacturers would develop from the supply disruptions and vehicle shortages. During this period, retained capital grew meaningfully from an already elevated starting point. Meanwhile, Subaru has strategically slow-played the BEV transition spending, presumably taking cues from its 21% shareholder, Toyota, which controversially but presciently took something of a wait and see approach to the BEV transition. The United States and Japan, which represent approximately 70% and 20% of Subaru’s volumes sold, respectively, have proven to be global outliers in terms of the slow pace of BEV adoption. Expectations of the amount of capital Subaru might be compelled to spend on BEV production are now being rethought and the timeline for such spending has been pushed back. Meanwhile, strong profitability continues to add to the cash pile.

Last year, in acknowledgement of these developments, the company began to increase shareholder distributions through dividends and buybacks until a trade war ensued. The company has temporarily retreated from buybacks, which we view as an excessively conservative choice, but has continued its dividend policy. As clarity around tariffs develops, or as the company makes operational adjustments to insulate itself, we expect that Subaru will again materially increase shareholder distributions. In our view, there can be no justification for the amount of capital currently being retained by Subaru, particularly for a company with a long track record of impressive profitability and exceptional returns on invested capital. For example, a policy to distribute as much as 100% of free cash flow, as adopted by other well-financed auto companies, would not even reduce the company’s pile of cash and investments, it would merely prevent it from growing even further.

In conclusion, one of my favorite Marty Whitman quotes was “the next time someone walks into this room with a perfect investment will be the first time,” which was communicated to our firm’s research department on occasion. Our Japanese investments are no exception. They are each imperfect in different ways, as all investments are. However, they are also very good businesses, are extremely well-financed, and trade at prices low enough to be more than reflective of their imperfections, in our view. Improvements could certainly be made in a few areas of corporate governance, which is why mounting pressure and widespread growth in shareholder engagement is so encouraging. All told, if the price one pays for an investment has a direct connection to the potential investment return and to the amount of investment risk being incurred, which it obviously does in our view, then the Japanese portion of the Fund today looks like a far better investment proposition than a great many alternatives.

QUARTERLY ACTIVITY

During the quarter ending June 30, 2025, the Fund initiated a position in Conduit Holdings Ltd (“Conduit”). The Fund also added to fifteen existing positions and reduced six existing positions. Cash holdings ended the quarter at 9.18%.

Conduit Holdings Limited is a Bermuda-based reinsurance company listed on the London Stock Exchange. Conduit launched as a newly formed company in January 2021 by raising $1bn of equity capital to deploy across property, casualty, and specialty lines. The business plan was to put that fresh capital, unencumbered by any legacy insurance liabilities, to work at the unusually attractive insurance rates prevailing at that time. In insurance terms, the idea was to take advantage of a “hard market” in certain lines of business.

At the outset, Conduit’s stated goals were to generate attractive underwriting profits, defined by the company as combined ratios in the mid-80% range, and returns on equity in the mid-teens across the insurance cycle. During its first few years of operation, much progress was made towards those corporate goals and towards the growth of underwriting premium volumes.

However, after generating strong results in 2023, Conduit experienced elevated loss events in 2024 and larger than expected loss exposure to the Los Angeles wildfires in 2025. In reaction, the company announced that it was purchasing multiple forms of additional reinsurance coverage to reduce earnings volatility throughout the remainder of the year. In addition, the CEO retired and was subsequently replaced by the Executive Chairman, who is also Conduit’s founder.

Over the course of these events, the valuation of Conduit shares declined significantly, and the Fund was able to initiate a position at a significant discount to book value. Notably, the company has no debt or off-balance sheet forms of financing and a high quality, low duration investment portfolio. Going forward, our expectation is that management should be able to stabilize profitability and regain the trust of investors. Should management succeed on these fronts, the shares would likely garner a higher valuation relative to book value, in our view. In our analysis, the combination of book value per share compounding and a reasonable increase in valuation would likely lead to an attractive investment outcome. Should the company valuation remain depressed, it is not inconceivable that management could consider a range of options to close the discount, especially given the strong financial alignment with shareholders created by Conduit’s management incentive plans.

Thank you for your confidence and trust. We look forward to writing again next quarter. In the interim, please do not hesitate to contact us with questions or comments at clientservice@thirdave.com.

Sincerely,

Matthew Fine

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of June 30, 2025 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: July 16, 2025

1 The MSCI World Index is an unmanaged, free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of 23 of the world’s most developed markets.

2 The MSCI World Value Index captures large and mid-cap securities exhibiting overall value style characteristics across 23 Developed Markets (DM) countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield.

3 The MSCI World Small Cap Index captures small cap representation across 23 Developed Markets (DM) countries*. With 3,908 constituents, the index covers approximately 14% of the free float-adjusted market capitalization in each country.

4 The S&P 500 Index is widely regarded as the best single gauge of large-cap U.S. equities. The index includes 500 leading companies and covers approximately 80% of the available market capitalization.

5 The S&P SmallCap 600® seeks to measure the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable.

6 All statistics in this paragraph have been calculated on a weighted average basis using the most recently reported financial data and quarter end portfolio weights.

For the Third Avenue Glossary please visit here.

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance, please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the Fund’s Institutional, Investor and Z share classes is 1.19%, 1.44% and 1.13% , respectively, as of March 1, 2025.

The fund's investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting www.thirdave.com. Read it carefully before investing.

Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through '40Act mutual funds and customized accounts. If you would like further information, please contact a Relationship Manager at:

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.