Notice

Notice

Small-Cap Value Fund Q126

Dear Fellow Shareholders,

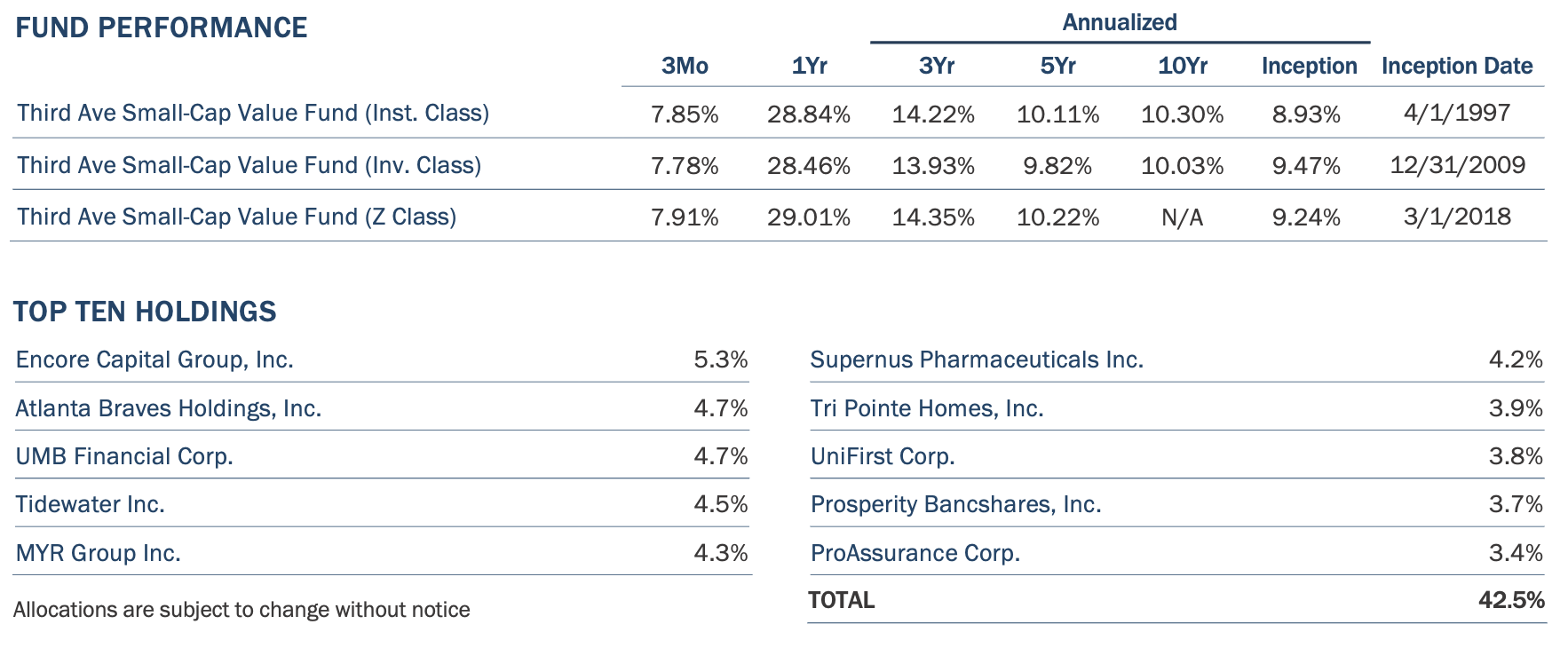

The Third Avenue Small-Cap Value Fund (the “Fund”) returned 7.85% during the first quarter of 2026, as compared to a return of 2.93% for the MSCI USA Small Cap Value Index (the “Index”)1. For the trailing three-year and five-year periods, the Fund produced annualized returns of 14.22% and 10.11%, respectively, as compared to 12.97% and 7.28% for the MSCI USA Small Cap Value Index.

PERFORMANCE DETAIL

During the quarter, Fund performance was aided by strong contributions from fertilizer producer LSB Industries, offshore energy services company Tidewater, consumer debt collection business Encore Capital Group, refinery operator PBF Energy and homebuilder Tri Pointe Homes, among others. On the other hand, negative performance contributions were produced by insurance business Octave Specialty Group, pharmaceuticals company Collegium, government and commercial consulting company ICF International, landowner and developer Five Point Holdings and property title insurer Investors Title, among others.

The Fund produced strong absolute and relative performance during the period despite a healthy list of investments on both the positive and negative sides of the ledger. Anecdotally, we have certainly felt an increased prevalence of stock winners and losers within the Fund and across U.S. equities more broadly. Some quantitative measurements specific to U.S. small-cap equities have begun to show signs of rising dispersion of returns among stocks, though measurements of performance dispersion today remain far more elevated for large-cap equities than for small-cap equities. That said, in both cases, small-cap equities and large-cap equities have lately shown far higher dispersion of returns than during the darker days of value investing from 2015 through 2021.

Furthermore, small-cap equities have broadly begun to show a bit of relative strength over the last year or so after more than a decade of relentless degradation relative to large-caps. Yet notwithstanding significant small-cap outperformance relative to large-caps over the last twelve months, small-caps remain exceptionally inexpensive compared to large-caps by historical standards. Each of these phenomena, broad and extreme small-cap relative cheapness, recent small-cap outperformance and rising dispersion of U.S. stock performance are important conditions that, in our view, improve the probabilities of outperformance for an active, fundamental, small-cap value strategy. In other words, when most stocks perform very similarly and small-cap stocks consistently perform poorly relative to large-cap stocks, it is very challenging to produce appealing returns and outperformance. Conversely, in an environment in which there are winners and losers to choose from, and small-cap stocks cease to consistently underperform, or maybe even begin to outperform on a path towards normalization of valuation relative to large-caps, there should be opportunities to outperform.

In review of first quarter Fund performance, one aspect that we find pleasing is that the Fund outperformed relevant indices during two highly distinct operating environments. The period leading up to U.S. and Israeli military action in Iran was decidedly positive for the Fund and relevant indices, though more so for the Fund. The onset of war brought fear, disruption and defensiveness that led to a performance decline for the Fund and relevant indices, though less so for the Fund. Across those experiences we sense the influence of both the investment approach itself and the way in which the portfolio is composed.

PORTFOLIO COMPOSITION & STRATEGY

While the Fund employs a concentrated approach to portfolio management, our team strives to construct a portfolio driven by a range of return drivers as well as risks. Variegation of returns is a bit of fancy jargon that some would use here. Our effort to accomplish this must go well beyond high-level industry classifications, and it includes quantitative and qualitative considerations built upon understanding of underlying businesses and the people involved. Some banks benefit from higher rate environments while some are harmed. Some financials, like those that lend on a floating rate basis (think private credit) may initially be aided by a higher rate environment but later harmed as the credit quality of borrowers is strained and a challenge to the floating rate lending model is exposed with a lag, for example. It is a mistake to make generalized assumptions about how financials or industrials will fair in one type of environment or another. Within the Fund, our energy-related business reacted to Middle East turmoil during the quarter in highly idiosyncratic ways, which we discuss below. On the qualitative front, evaluation of decision-makers, their strategies and their incentive structures are a very important part of our strategy broadly, given the emphasis we place upon the potential for shareholder wealth creation through resource conversion, ultimately contributing to the strength of absolute performance. It is also an important part of producing idiosyncratic (or variegated) return streams within the Fund.

The Fund holds several positions that, under typical operating conditions, do reasonably well earning decent margins and satisfactory returns on capital. That description doesn’t necessarily make them fabulous businesses though they can be fabulous investments depending upon the price one pays for the investment. Normal operating conditions for many businesses that are complex and global are characterized by smooth trade flows, ease of imports for input goods, price stability of inputs and the like. Some types of businesses, however, benefit from disruption and go from doing alright in normal times to earning very attractive returns in periods of disruption. The combination of doing alright in normal times and doing extremely well occasionally can create an attractive and idiosyncratic return stream to owners of the business.

Obviously, this most recent quarter was not business as usual with elevated U.S. import restrictions and rapidly rising energy costs, which are inputs for most businesses. Leading performance contributor LSB Industries benefited from global gas disruption, rising prices and potentially serious impacts to the global fertilizer supply. Disruption to Middle East oil and gas flows and damage to Middle East processing assets creates significant disruption to energy and product flows, though to varying degrees and depending on location, which means wider pricing differentials and wider crack spreads for those positioned to take advantage. The currently disrupted environment is very desirable for refining company PBF Energy in many ways. SandRidge Energy, an oil and gas producer, was also a beneficiary of rising disruption to Middle East energy transportation during the quarter and has the most direct connection to higher energy prices. Kaiser Aluminum is also a beneficiary of impediments to U.S. metal imports. All four investments performed well during a quarter which was marked by disruption to normal operations of their respective industries.

However, while SandRidge Energy is a direct beneficiary of price increases and PBF Energy mostly benefits from price volatility and price differentials, our third energy-related holding Tidewater was only an indirect beneficiary of disruption and higher energy prices during the quarter. In fact, as an offshore services company, disruption to business as usual in the Middle East may have some modest short-term negative implications for Tidewater though in the longer-term we think a rising global focus on energy security is very positive for Tidewater. While Tidewater was a leading contributor to performance during quarter, the vast majority of the return occurred before U.S. military action in Iran. Tidewater performed particularly well in response to its acquisition of a fleet of Brazilian supply vessels, a well-conceived, countercyclical business building transaction and the third such transaction Tidewater has executed upon in recent years. This brings us back to the idiosyncratic return streams driven by episodic resource conversion activity within the Fund.

Tidewater’s acquisition was one of three significant transactions announced by Fund holdings during the quarter. After an extremely long and contentious courting period, long-time Fund holding Unifirst finally agreed to be acquired by much larger competitor, Cintas. As we described at length in a previous letter, the Cintas offer was very attractive from the perspective of a Unifirst shareholder. We were pleased that the board accepted the offer in recognition that the purchase price exceeded any level of shareholder wealth they were likely to be able to create independently and that Cintas was uniquely situated to pay full price. During the quarter, Tri Pointe Homes also agreed to be acquired by Sumitomo Forestry, one of several Japanese homebuilders that have been making increasing forays into the U.S. homebuilding market. Again, we felt the price paid was attractive and were supportive of the sale.

While culminating successful investments, either through simple price appreciation or through resource conversion activity is gratifying, we are then presented with the opportunity and challenge of recycling Fund capital. Here too, higher dispersion of equity price movements, meaning the presence of winners and losers, is a helpful condition for redeploying Fund capital and, for better or worse, there is almost always a crisis going on somewhere. The “always a crisis going on somewhere” truism tends to manifest in a continuum of rolling pockets of opportunity that attract our analytical attention. The approach is not to be reflexively contrarian but to try to decipher, through fundamental analysis, experience and judgement, which areas of pessimism rise to the level of excess or unreasonableness and, therefore, have produced security prices that represent asymmetric investment opportunities, probabilistically speaking. In recent periods, several such rolling pockets of opportunity have been fruitful sources of opportunity:

During 2025, Liberation Day tariff fears led to an investment in auto supply company Visteon and additions to an existing investment in agricultural equipment maker Alamo Group. Meanwhile, a continuing slowdown in new residential construction compounded woes from a longer running dearth of existing home transactions, which drives renovation activity, leading to a severe recession for residential building products. The Fund initiated investments in BlueLinx and Boise Cascade in response. Fears of regulatory changes that may result from the 2025 New York City mayoral election led to acute pessimism for banks with loan books exposed to rent-regulated properties, creating the opportunity to initiate a position in Flagstar and for existing holding OceanFirst to grow materially through the acquisition of Flushing Financial.

Most recently, during 2026, the proliferation of artificial intelligence technologies is causing widespread fears of disintermediation and obsolescence risk in labor and software markets, among many others. This has been an important part of creating winners and losers and broad performance dispersion in public equity markets. In our view, this has been helpful in contributing to an unusually high level of investment activity during the quarter.

ACTIVITY

During the quarter, the Fund initiated positions in five new holdings, Qualys, Inc., Compass, Inc., Harley-Davidson, Inc., Catalyst Pharmaceuticals, Inc. and Robert Half Inc. The Fund exited its position in Cantaloupe Inc, which is in the process of being acquired in a transaction expected to close imminently. The Fund also trimmed several high performing positions, some of which are discussed above, and generally redeployed cash into new positions and several existing holdings that have performed less well of late.

Qualys, Inc (“Qualys”) is an established, growing, and highly profitable cybersecurity company and the largest of three leading specialized vendors of vulnerability management software. Qualys was among the first to build a cloud security platform and has continued to improve its offerings and applications. Its highly regarded software solutions, which identify and repair vulnerabilities to cyber threats within customer networks, are well utilized by a majority of Global 500 corporations.

The recent equity market dislocation of wide swaths of the software industry has provided an opportunity for the Fund to invest in a very well-financed business that appears well positioned to not only survive but potentially thrive in the new A.I. environment. As we often say when talking about companies weathering uncertainty, it starts with the balance sheet. Qualys is undeniably well financed, with no debt and a cash war chest of nearly $700 million, relative to its $3 billion market capitalization. The company has demonstrated a long history of disciplined profitability and methodical platform expansion, balancing revenue growth with high margins and robust operating and free cash flow generation. At recent share prices, current profitability would suggest a free cash flow yield in the double-digits.

While the pace of potential disruption is inherently uncertain, we do take comfort in the fact that large swaths of Qualys customer base come from highly regulated sectors such as finance and healthcare, which maintain regulatory statutes that demand the use of third-party vulnerability management providers such as Qualys.

Further, there is a school of thought that increasing use of agentic A.I. may ultimately increase the need for accuracy, accountability and regulatory compliance of IT environments, which could ultimately support demand for Qualys’ services. The proliferation of generative A.I. agents being rolled out creates more openings for bad actors to exploit insecure software and appears likely to dramatically increase the number of devices that companies will need to monitor to ensure a safe IT environment.

Harley-Davidson, Inc. (“Harley-Davidson”) manufactures motorcycles and accessories, sells financial services and earns licensing revenue. While its brand remains iconic, its core motorcycle market in the U.S., and the heavyweight bikes in which Harley-Davidson specializes, have suffered several years of sales declines. Some recent declines are attributable to the demand pull-forward that occurred during COVID, though demand for new heavyweight bikes has been stagnant-to-declining for years. For Harley-Davidson specifically, the last several years have also been marked by multiple activist campaigns, board turnover, management changes and string of strategic missteps.

One central strategic misstep, which represented a priority for previous management, included a virtual exit from lower priced entry level bikes, in favor of more expensive and higher profit margin bikes. While conceptually appealing, that strategy ignored the need to attract new entry-level customers and that entry-level bike purchases create incremental demand for high margin customizations, branded accessories and financial service contract originations. Possibly most important, however, was a lack of recognition that stuffing dealerships with far more big expensive bikes than are in demand is bad for dealer economics, creates dealer frustration and discontent and ultimately results in significant price discounting to clear stale excess inventory.

Further, Harley-Davidson’s electric motorcycle venture, LiveWire, has been a significant drag on Harley-Davidson since its birth and electric motorcycle sales have fallen stunningly short of expectations. As recently as 2022, LiveWire had projected it would sell more than 50,000 electric motorcycles in 2025 but ultimately achieved only about 1% of that volume target. Because Harley Davidson owns nearly 90% of publicly-traded LiveWire, significant operating losses remain consolidated within Harley-Davidson’s financial statements, creating a very significant optical drag on Harley-Davidson’s operating performance. Harley-Davidson has been providing ongoing support to sustain the business, though management has indicated that LiveWire has received its final financial lifeline from the company. A solution that disentangles the consolidation of the two companies, such as the eventual insolvency of LiveWire, would remove the optical drag on Harley-Davidson’s operating profits and the distractions of a failing non-core business. We view an eventual LiveWire insolvency as highly probable.

On a more positive note, last year, Harley-Davidson’s Financial Services (HDFS) business was able to release a very substantial amount of capital through a creative transaction in which it sold a substantial portion of its existing financial receivables and created a future flow agreement for most of its retail motorcycle loans to partners KKR and PIMCO. Harley-Davidson also sold a 4.9% equity stake in HDFS to each partner and will retain roughly one-third of new retail loan originations going forward. HDFS will also receive ongoing loan servicing fees from its partners. The proceeds from the transaction enable Harley-Davidson to further invest in manufacturing operations and continue returning capital to shareholders. The new structure of HDFS will operate with less capital intensity, more fee generation and higher returns on capital. The transaction also highlights the underlying value of HDFS, which has historically been underappreciated by the market.

Our sense is that elements of the strategy changes being implemented by new management create the opportunity for far better operating performance from the core motorcycle business and it is clear that significant progress has already been made in clearing older inventory from dealership floors. It is also notable that, despite manufacturing 100% of its bikes for the U.S. market in its Wisconsin and Pennsylvania plants, tariff expenses have created a major financial headwind for Harley-Davidson. While we can’t say when this situation may improve, a very substantial tariff expense is yet one more headwind facing Harley-Davidson today, which may not prove to be permanent. Harley Davidson plans to detail its operational improvement strategy later this year, positioning the company for a return to sustainable growth and profitability. While there’s urgency to finally put the company back on the right path, Harley-Davidson is afforded flexibility from a sizeable net cash position in its industrial operations. Market expectations remain very low, with the company’s shares trading at a sizeable discount to tangible book value and a modest multiple of very depressed earnings.

Compass, Inc. (“Compass”) is a technology enabled residential real estate brokerage focused on the luxury and upper-middle segments of the U.S. housing market. The company operates a national platform that combines the nation’s largest agent network with proprietary software tools designed to enhance productivity, client engagement and transaction efficiency. Under this business model, agents are independent contractors who generate commissions on the purchase and sale of a home and revenue is generated primarily from commissions on home sales.

U.S. existing home sales are at historically depressed levels, with U.S. residential transactions at their lowest levels on a per capita basis in 60 years. Compass has been pressured by a combination of higher mortgage rates, affordability challenges and constrained housing inventory, weighing on transaction volumes and commission revenue across the industry. At the same time, investor uncertainty has arisen around the long term economics of residential brokerage, fears of commission compression, heightened agent competition and potential technological disintermediation. On the other hand, Compass’ recent transformational merger with Anywhere Real Estate creates the largest residential real estate platform globally, expands Compass’s agent and brand footprint and diversifies revenue through recurrent high margin franchise, title, escrow, and relocation revenue streams.

We expect the industry will continue to move towards a structure in which there are several dominant platforms that effectively serve as exchanges for residential transactions. Compass is very well positioned to emerge as one of those dominant exchanges capitalizing upon the strength of the company’s digital search platform combined with a leading selection of property listings facilitated by its increasing agent count. As transaction volumes eventually normalize, we believe Compass will achieve significant profitability, demonstrating the work that both standalone Compass and Anywhere had done pre-merger to achieve substantial cost savings in recent years. Given the inherent operating leverage of the business model, any increase in transaction volumes would meaningfully improve profitability.

Catalyst Pharmaceuticals, Inc. (“Catalyst”) is a biopharmaceutical company that has achieved long-running profitability and a sizeable and growing cash balance. The company embodies what our team sometimes refers to as an owner-operator approach through its buy-and-build strategy to create long-term shareholder wealth by acquiring and integrating orphan-designated assets, typically from smaller biotech companies that lack the financial resources to support a successful new drug launch. In short, the company’s business model begins after the research and development stage, supporting bring-to-market strategies for significantly derisked products. Catalyst’s specialties are market analysis, patient identification and drug commercialization.

Today, Catalyst’s most significant growth asset is a drug called Firdapse, which is the only approved drug in the U.S. to treat LEMS (Lambert-Eaton Myasthenic Syndrome). Firdapse appears to have considerable runway over the next nine years to potentially double its treated patient population. A very favorable reimbursement environment, high awareness among physicians and strong clinical data has set up an inflection point for Catalyst's Firdapse commercialization efforts.

We believe Catalyst’s current modest valuation reflects a lingering lawsuit with Hetero USA, Inc., a generic manufacturer. Catalyst has prevailed multiple times in defending its intellectual property against three other generic manufacturers including Teva Pharmaceuticals, Inventia Healthcare and Lupin Pharmaceuticals, while the U.S. Court of Appeals for the 11th Circuit has ruled in favor of Catalyst intellectual property rights. The only remaining patent case pending, against Hetero, has a tentative trial date set for May 2026. We think a favorable trial outcome or settlement in line with the Catalyst’s settlements in previous challenges, which have preserved Catalyst’s exclusivity to February 2035, would represent a clearing event for a meaningful overhang for the company.

Catalyst has built a very strong cash position, with no debt on the balance sheet and robust cash flow. This should continue to support their strategy of buying products to bolster scale. The company continues to work to develop additional indications for its three commercial products with a few indications that could provide for low-risk and high-upside payoffs. Equally, Catalyst continues to benefit from a game-changing development announced in August 2025 when Firdapse was formally written into the standard of care Clinical Practice Guidelines for the National Comprehensive Cancer Network (NCCN). By working with several rare disease advocacy organizations to help increase awareness and support for patients living with LEMS, the company has the opportunity to significantly expand its patient population and grow revenues at a mid-teens rate.

Robert Half Inc. (“Robert Half”) is a professional staffing company specializing in temporary placements in the fields of finance and accounting, technology, and administrative and customer support. Robert Half also operates Protiviti, which provides consulting in a variety of fields including risk management and internal audit. The U.S. staffing industry has experienced three consecutive years of muted activity following a period of unusually strong labor demand during and after the pandemic, when U.S. unemployment fell to multi-decade lows. As companies adjust to excessive prior hiring of permanent employees, the use of temporary labor has suffered a significant cyclical decline, leaving temporary workers at a historically low share of the overall workforce.

Beyond cyclical pressures, current investor concerns center on the potential for artificial intelligence to reduce demand for certain roles and automate aspects of the recruiting process. An alternative view holds that disciplines such as tax and audit require considerable professional judgment and risk assessment that extend beyond historical data and rules-based implementation, sustaining the need for human expertise. Further, proprietary information relating to individual temp employee performance in various roles, which has been accumulated by the likes of Robert Half over decades, may prove to be a valuable asset to employers in a world in which A.I. renders it difficult to discern what is real. Additionally, although barriers to entry in staffing may seem low, Robert Half benefits from an extensive two-sided professional network, long-running proprietary candidate data and expertise in matching specific skill sets to defined client needs. The company’s shares trade at a low single-digit multiple of normalized cash flow. The company has generated positive annual free cash flow for more than three consecutive decades and has consistently returned the majority of that cash to shareholders through dividends and share repurchases. The company’s dividend, which, at the present share price, offers a near-double-digit yield, is currently supported by ongoing cash generation.

Robert Half is extremely well-financed with a debt-free balance sheet and a substantial cash balance. The nature of the company’s business requires very little capital-intensity, and the company continues to produce a material amount of free cash flow, even in deeply depressed operating conditions. Management continues to strategically retain experienced recruiters despite near-term earnings pressure, recognizing that new recruiters require approximately two years to reach average productivity, and that the ability to retain recruiting staff in a cyclically depressed environment represents a strategic competitive advantage. There are also signs that Robert Half and a few industry peers have increased efforts to hire additional recruiters in anticipation of an eventual cyclical upturn.

CONCLUSION

For those interested in learning more about the Third Avenue Small-Cap Value strategy, we have produced a brief video discussing our approach. The video focuses on balance sheet quality and price consciousness, the role of resource conversions and contrarianism within our strategy, and how portfolios are constructed with prudent concentration. The video can be found on the Third Avenue website under Resources, in the News and Media tab.

Please don’t hesitate to contact us with any questions or comments at clientservice@thirdave.com. Thank you for your continued confidence and trust.

Sincerely,

The Third Avenue Small-Cap Value Team

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of March 31, 2026 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: April 16, 2026

1 The MSCI USA Small Cap Value Index captures small cap securities exhibiting overall value style characteristics across the US equity markets. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. The index is not a security that can be purchased or sold.

For the Third Avenue Glossary please visit here.

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the Fund’s Institutional, Investor and Z share classes is 1.26%, 1.51% and 1.20%, respectively, as of March 1, 2026.

Risks that could negatively impact returns include: fluctuations in currencies versus the US dollar, political/social/economic instability in foreign countries where the Fund invests, lack of diversification, volatility associated with investing in small-cap securities, and adverse general market conditions.

The fund's investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting www.thirdave.com. Read it carefully before investing.

Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through '40Act mutual funds and customized accounts. If you would like further information, please contact a Relationship Manager at: