Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

Notice

Third Avenue Management is aware of recent incidents involving unauthorized individuals and groups falsely claiming to represent Third Avenue Management and its affiliates through social media platforms, messaging applications, email, and fraudulent websites. In some cases, these bad actors have used the names, photographs, or identities of Third Avenue employees in an attempt to appear legitimate.

These individuals and websites are not affiliated with, sponsored by, or endorsed by Third Avenue Management.

Third Avenue Management does not solicit investments, provide investment recommendations, or request personal or financial information through social media platforms or messaging applications such as WhatsApp, Telegram, Signal, or similar services.If you receive a suspicious communication claiming to be from Third Avenue Management, we encourage you to verify its authenticity before responding or providing any personal or financial information. If you are unsure whether you are communicating with an authorized representative of Third Avenue, please contact us directly using the contact information available on our official website.

Third Avenue Management, its affiliates, directors, officers, employees, and agents are not responsible for communications, representations, or activities conducted by unauthorized third parties. If you believe you have been the target of an impersonation or investment scam, or that you or someone you know has been a victim of fraud, please contact your local law enforcement agency and report the incident to the appropriate authorities. In the United States, suspected internet fraud can also be reported to the Federal Bureau of Investigation's Internet Crime Complaint Center (IC3) at https://www.ic3.gov/.

These individuals and websites are not affiliated with, sponsored by, or endorsed by Third Avenue Management.

Third Avenue Management does not solicit investments, provide investment recommendations, or request personal or financial information through social media platforms or messaging applications such as WhatsApp, Telegram, Signal, or similar services.If you receive a suspicious communication claiming to be from Third Avenue Management, we encourage you to verify its authenticity before responding or providing any personal or financial information. If you are unsure whether you are communicating with an authorized representative of Third Avenue, please contact us directly using the contact information available on our official website.

Third Avenue Management, its affiliates, directors, officers, employees, and agents are not responsible for communications, representations, or activities conducted by unauthorized third parties. If you believe you have been the target of an impersonation or investment scam, or that you or someone you know has been a victim of fraud, please contact your local law enforcement agency and report the incident to the appropriate authorities. In the United States, suspected internet fraud can also be reported to the Federal Bureau of Investigation's Internet Crime Complaint Center (IC3) at https://www.ic3.gov/.

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.

March 31, 2025

Small-Cap Value Fund

Small-Cap Value Fund Q125

Dear Fellow Shareholders,

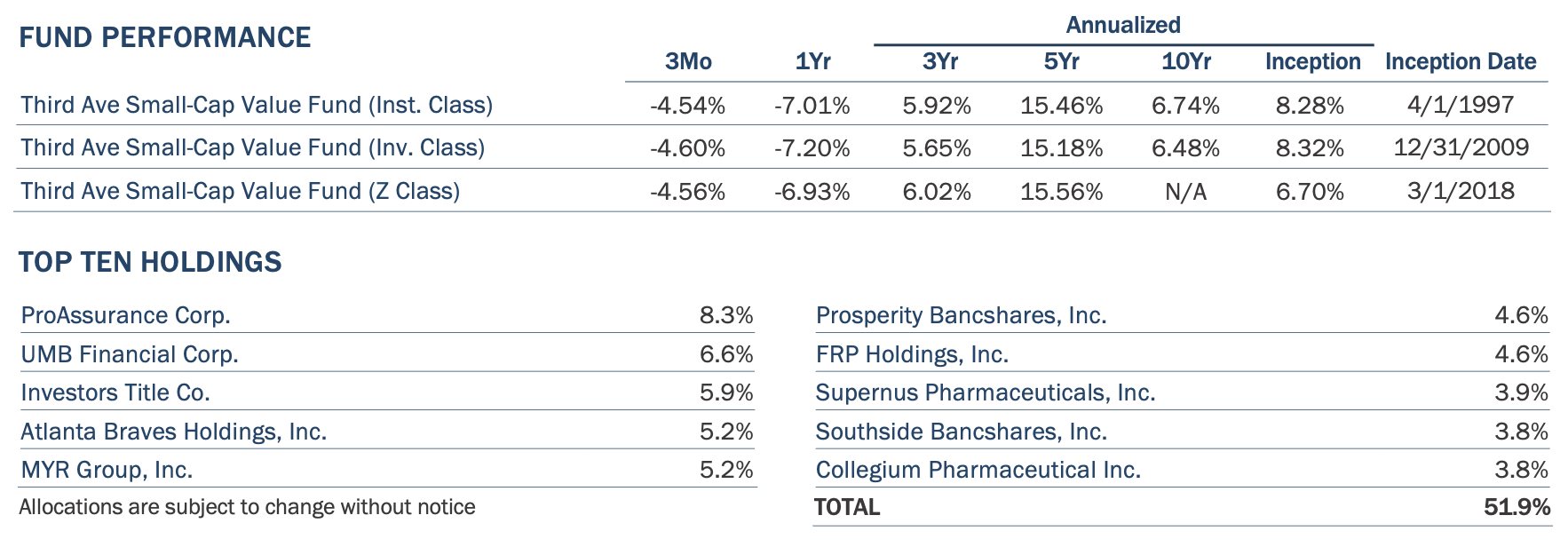

The Third Avenue Small-Cap Value Fund (the “Fund”) returned -4.54% during the first quarter of 2025, compared to a return of -5.87% for the MSCI USA Small-Cap Value Index (the “Index”)1 and a return of -7.74% for the Russell 2000 Value Index2. For the trailing five-year period the Fund has returned +15.46%, annualized.

PERFORMANCE REVIEW

Performance during the quarter was led by positive contributions from a wide range of individual businesses and idiosyncratic developments. In March, specialty insurance provider ProAssurance announced that it has agreed to a takeover offer from The Doctor’s Company. At $25 per share, the purchase price represents an approximate 60% premium to the pre-offer trading price, highlighting the value that was embedded within the shares and leading to ProAssurance generating the single largest contribution to quarterly Fund performance. Homebuilder FivePoint Holdings (“FivePoint”), appliance manufacturer Hamilton Beach Brands, agricultural conglomerate Seaboard and entertainment company Atlanta Braves Holdings, among others, also made important contributions to performance. In the case of FivePoint, the company’s year-end 2024 report was released in January, highlighting a high volume of sales of home sites at its two primary development communities, Valencia and Great Park. The volume of transaction activity and the transaction prices further highlighted the value of FivePoint’s land holdings in highly desirable communities in severely land-constrained areas. The sizeable transaction proceeds further fortified the company’s balance sheet and liquidity for further development activity. With regard to Atlanta Braves Holdings, the company reported several pieces of positive news during the quarter relating to both its real estate development assets as well as multiple new media and streaming rights agreements. Entities controlled by John Malone, Atlanta Braves Holding’s controlling shareholder, could also be seen consistently buying shares throughout the quarter.

Meanwhile, detractors from performance this quarter included construction and engineering company MYR Group, consumer finance company Encore Capital Group, research and consulting company ICF International, offshore oil & gas services provider Tidewater, and regional bank UMB Financial. Tidewater represents an interesting case study. In recent quarters, the company has been a poor performer and one of the larger drags on Fund performance. As recently as a year ago, the company had been a star performer for the Fund and was benefiting from a strong tightening of the supply and demand balance for global offshore support vessels. In that environment, with a favorable outlook and far higher share prices, the Fund sold a material portion of its Tidewater shares. It is notable that several growth-oriented funds filed as significant new shareholders around the time of the Fund’s sales. As an investment approach, we tend to buy grey clouds and sell sunshine and that period was starting to look like sunshine in the sense that the share price was increasingly reflective of the very positive near-term outlook.

However, outlooks change and, to the extent one has purchased an investment at prices reflective of a very favorable outlook, a deterioration of that outlook can be very painful. Since the second half of 2024, several large offshore projects have been temporarily delayed, limiting the immediate demand for more offshore service assets. While the current consensus forecast for Tidewater’s 2025 operating performance is roughly flat compared to 2024, the share price has seen a considerable decline. We continue to believe that the long-term industry dynamics - marked by virtually no new supply of offshore service vessels for the foreseeable future, gradually declining supply of the existing global vessel fleet through aging and attrition, along with increasing long-term demand - are very much intact. Our job, as we see it, is to estimate the value of businesses, across a range of scenarios, and with a good bit of conservatism baked in, and then try to seize opportunities to buy them at significant discounts to those estimated values. Our view is that Tidewater’s share price decline represents a large overreaction to the softening of its near-term outlook and the Fund has once again begun to grow its Tidewater holdings.

CLOUDS OF VAGUENESS OVER SMALL-CAP LAND

"To me our knowledge of the way things work, in society or in nature, comes trailing clouds of vagueness.Vast ills have followed a belief in certainty, whether historical inevitability, grand diplomatic designs, or extreme economic policy. When developing policy with wide effects for an individual society, caution is needed because we cannot predict the consequences.”

- Kenneth Arrow

Similar to other major exogenous shocks to the global economy, such as the September 11, 2001 terror attacks, the Global Financial Crisis, and the COVID-19 pandemic, the launching of a global trade war presents a significant change in circumstances and a lot of unknowns. As was the case with each of those previous events, it is likely that no living professional investor has any first-hand experience with a global trade war. As was the case in each of those previous shocks, our reaction to the uncertainty is straight-forward. We are actively looking for opportunities at prices excessively reflective of the uncertainty. While stock volatility within small-cap stocks is often viewed as a bug, we simply view it as a feature, and one that helpfully increases the probability of stocks being materially mispriced, particularly during tumultuous environments.

In another interesting parallel, U.S. small-cap stocks have woefully underperformed U.S. large-cap stocks in recent years. We have repeatedly highlighted that fact, and the yawning relative valuation gap between the large and small companies, in these shareholder letters. In the years leading up to September 11, 2001, the dot-com bubble produced a very similar phenomenon of large-cap outperformance and a huge valuation spread relative to small-caps. Coincidentally, the most extreme points of relative valuation between U.S. large-caps and small-caps look almost identical in both instances. In other words, the last time valuation spreads between U.S. large-caps and small-caps were as wide as they have been during the last few years was more than two decades ago and the end of that period was punctuated by the bursting of the dot-com bubble followed by the September 11th terror attacks. In the years afterward, small-cap stocks went on to outperform by an enormous margin, not only reverting to a historical mean relative valuation, but shooting well beyond. Sometimes, exogenous shocks have a way of punctuating long-running trends and helping to remedy long-building distortions. We will stop short of a full speculation here, but it would not surprise us to see this period of turmoil, which is occurring at a time of multi-decade high valuation spreads between large-caps and small-caps, act as a form of punctuation.

As it relates to the presidential orders unveiled on what is now known as Liberation Day, the Third Avenue Value Fund shareholder letter engages in a more fulsome discussion of their advisability and potential implications. We will not repeat those comments here but, rather, focus on how the Third Avenue Small-Cap Value Fund is approaching this period of uncertainty and volatility, in a philosophical sense.

First, in academic finance, volatility is used as a proxy catch-all for any and all types of investment risk. Yet, no private owner or control investor of a business would ever think of business risk in this way. An owner of a business, which is the mindset with which we approach investing, uses adjectives to describe specific business risks, e.g., insolvency risk, obsolescence risk, competitive risk, currency risk, regulatory risk, etc. No business owner would ever forgo that form of specific and fundamental consideration and instead use “how volatile would the stock of my company be if I listed it in the public market?” as shorthand. What an owner of a business cares about is the risk of his capital becoming permanently impaired, not whether other people are optimistic or pessimistic about his business on any given day.

"The great emphasis on volatility in corporate finance we regard as nonsense.”

– Charlie Munger

Similarly, Warren Buffett has railed against the idea that a stock falling significantly would somehow make it a riskier investment because its measured historical volatility is now higher, even though the price one is paying is now much lower. In our view, the concept of volatility as a valid proxy for investment risk only resonates with short-term speculators, people who invest on margin, people who aren’t equipped to evaluate actual fundamental business risk, and people who completely ignore the very obvious direct relationship between the price one pays for a security and the investment risk being incurred. One of Marty Whitman’s most interesting insights, in our opinion, was that there is not necessarily a tradeoff between investment risk and reward for a fundamental, price-conscious investor as there is within the framework of academic finance. In other words, the cheaper you buy a business the lower your investment risk and the greater your potential investment return. Price changes the relationship between risk and reward and once an investor is free of the concept that volatility is risk, fear of the “random walk” of near-term price volatility tends to fade away.

"Under some circumstances, following a significant decline in price an asset actually becomes less risky, since it can be acquired more cheaply. The common-sense conclusion of bottom-fishing investors contrasts with the statistician’s conclusion that a dramatic drop in price increases observed (historical) volatility, implying a higher risk level for the asset.”

- David Swensen –Pioneering Portfolio Management

It would be reasonable at this point to ask, “if Buffet, Munger, Swensen, Whitman and other investing greats have achieved decades of success dismissing the concept of volatility as risk, why doesn’t everybody just follow that prescription?” The hard reality is that this approach to investing almost guarantees periodic underperformance and is, by definition, contrarian and, therefore, controversial at the time of investment. Within most asset management firms, controversial investments and periodic underperformance pose enormous professional and career risk to the investor. In our view, it is not a mistake that many asset management firms pursuing such approaches are either controlled by the investor or synthesize that governance somehow. It is hard to overstate how difficult it is to be a contrarian, fundamental, value investor, who ignores near-term volatility with a fund management company executive looking over your shoulder, possibly second-guessing your investing activity, which often looks reckless in the moment to non-contrarian investors. Today, at Third Avenue Management, our three-member management committee is entirely comprised of owners of the business who are also the most senior members of our portfolio management team. We feel no compulsion to limit tracking error or make the strategies as marketable as possible in the near-term. We want to foster thoughtful, well-founded, courageous investing and view this as a strategic long-term advantage.

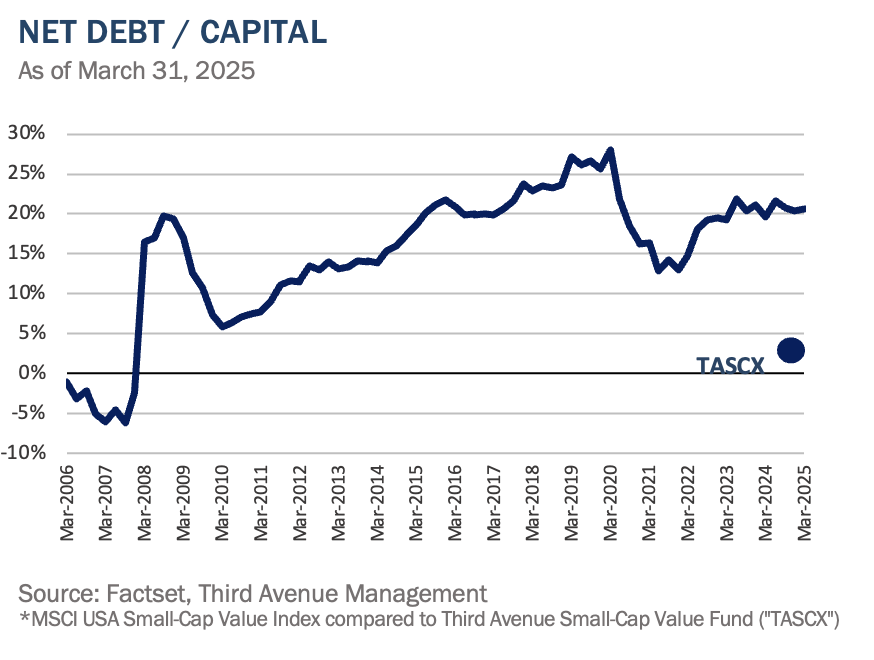

Second, an indispensable aspect of our approach is the determination to invest in well-financed businesses. It is most often the case that attractive contrarian investments are available because something has gone wrong and some type of headwind or challenging outlook prevails in the near-term. We strive to maintain a healthy level of humility in our investment approach, which precludes us from predicting a specific timeline over which the headwinds will dissipate. Therefore, it is a prerequisite, in any investment environment, that we focus our investment activity on well-financed businesses. This is glaringly obvious when one looks at the financial leverage statistics of the Fund, as compared to a passive index, for example. The idea is that the companies we own can survive for long periods of time in difficult circumstances without running short of liquidity and needing to conduct value-destructive actions, like equity issuance or asset sales at the worst possible times. Clearly, the outbreak of a tariff war, already leading to observable disruptions to some supply chains, consumer buying patterns, and a number of industrial input prices is creating a high level of uncertainty and could ultimately lead to a recession. Further, it remains unclear whether sweeping U.S. import tariffs will be waved away by the end of the week or whether they will persist for years. In our view, the benefits of owning well-financed companies, as standard operating procedure in one’s investment activity, is made most apparent in difficult periods. This period is not different in that regard.

"I think it’s easier than trying to play the market and forecast the market’s gyrations. Most investors are outlook-conscious. I’m price-conscious. I have this easy way of measuring price, quantity and quality. Everything is in the balance sheet–the only way you know whether you’ve covered all the bases is to look at the balance sheet.”

- Marty Whitman

Third, in the context of Third Avenue Management investment analysis it is common to analyze potential investment outcomes over a three-to-five-year investment horizon. Ours is inherently a long-term approach. As a practical matter, historical Fund turnover shows that average investment holding periods have matched that time horizon fairly well. Again, in the normal course of Third Avenue investment activity, it is very common for the Fund to purchase a business with a clouded, or even overtly negative, near-term outlook. Cyclical depressions or fundamental business challenges generally do not abate overnight. So, in addition to balance sheet strength, a long-term investment horizon is a simple necessity of the approach. It is notable then that our typical investment time horizon spans beyond this presidential term. It seems reasonable to expect that the path forward from Liberation Day will be circuitous and possibly surprising at times. This may produce more stock price volatility, though businesses with strong balance sheets do have a powerful bulwark against actual fundamental business risk, as distinct from stock volatility. All of that said, it is our team’s view that many of the intents of the Liberation Day orders are unachievable in a practical sense. We are hopeful that economic rationality will prevail. It is encouraging that a 90-day pause was implemented only one week after we were “liberated” and that many individuals involved in trade negotiations have intimated that the successful negotiations could bring a swift elimination of import tariffs. While it is impossible to predict when this form of uncertainty will be reduced, we certainly believe we are in a position to endure beyond it. Given the extent to which U.S. small-cap stocks presently reside in a valuation range of extreme cheapness, relative to U.S. large-caps, some abatement of tariff uncertainty could provide a powerful impetus for a reduction of that historic valuation spread.

"…not everyone worries about volatility. Even though risk means more things can happen than will happen – a definition that captures the idea of volatility – that statement specifies no time dimension. Once we introduce the element of time, the linkage between risk and volatility begins to diminish. Time changes risk in many ways, not just in its relation to volatility.”

- Peter L. Bernstein –Against the Gods,

The Remarkable Story of Risk

EMERGING FROM THE VAGUENESS

As discussed in many prior letters, we are attempting to identify securities which are available in the public markets, at valuations significantly below their private market value, with a low probability of permanent capital impairment over our long-term investment horizon. Those same attributes often do attract acquirers of our businesses, be they strategic acquirers, private equity buyers, or privatizations. With smaller-capitalization companies trading at extremely low valuations compared to larger companies, the potential energy built up in small-cap merger and acquisition (“M&A”) activity seems substantial. Our previous letter also flagged a strong White House will to deregulate as well as the potential for corporate tax cuts. Either agenda could be viewed as a potential economic boost, particularly as policy makers grapple with the implications of the trade war. It is common for many U.S. small-cap companies to be domestically focused and often less globally integrated. Those are traits which seem likely to increase the probability of a transaction at the present moment. It is possible that the combination of these features could accelerate a nascent wave of small-cap transaction activity.

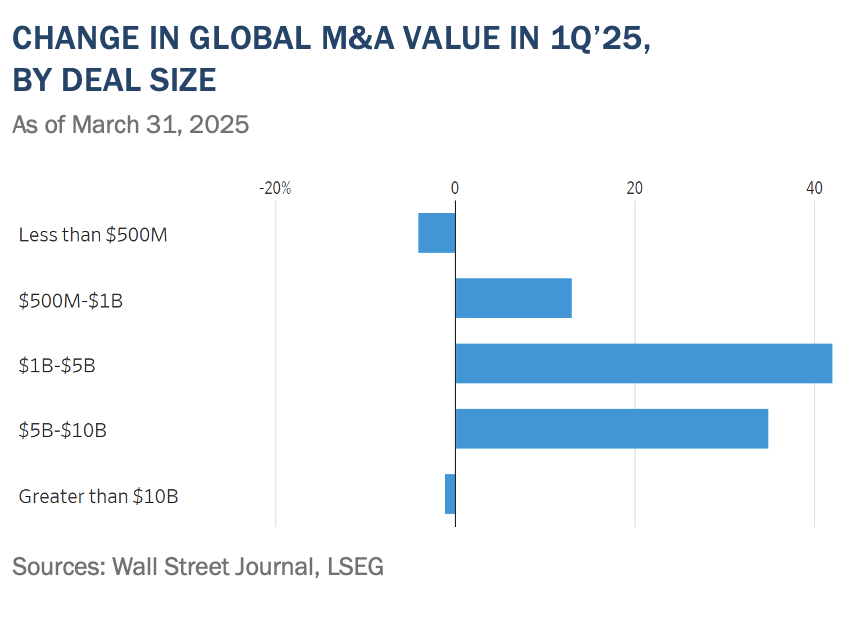

For example, The Wall Street Journal’s April 2, 2025 article, titled The M&A Boom Wall Street Wanted Is Here, if You Know Where to Look explains that Wall Street’s visions of a deal bonanza under President Trump haven’t yet materialized. However, the article goes on to explain that relatively smaller deals are having their best start to the year since 2021. During the first quarter, the total deal value for transactions in the $1 billion to $10 billion range increased 42% from a year earlier, according to data from the London Stock Exchange Group, while the number of deals grew by nearly 36%.

As we described earlier in this letter, Fund performance during the quarter was propelled by M&A activity when ProAssurance, a domestically-focused insurance company, was acquired in an industry-consolidating transaction. We view the large premium of the offer price to be indicative of the undervaluation present in certain areas of the small-cap universe.

ACTIVITY

During the first quarter the Fund engaged in a heightened level of activity as the prospect of sweeping U.S. import tariffs came to be openly discussed. The Fund’s activity has further accelerated post the Liberation Day announcements and subsequent equity market declines. During the quarter, the Fund initiated a position in BlueLinx Holdings (“BlueLinx”) and added to holdings in OceanFirst Financial, Ambac Financial, ICF International, and Tidewater. The Fund also reduced holdings in a number of positions. The net effect of Fund activity reduced the Fund’s cash position to 3.58%, from 8.00% the prior quarter.

BlueLinx Holdings Inc. (“BlueLinx”), is a distribution business, acting as an intermediary between the manufacturers of finished residential and commercial building products - such as siding, millwork, and specialty lumber panels - and product retailers and professional contractors in local markets. The company's key assets enabling its distribution capabilities are a nationwide footprint of 65 warehouses, storage facilities, and logistics assets. The company has seen its stock decline meaningfully in recent quarters in anticipation of a perceived slowdown in U.S. housing and potential disruptions to the supply of imported building products.

Although the company has narrow operating margins typical of many distribution businesses, BlueLinx has a strong track record of generating attractive free cash flow as a public company. Further, the company maintains a net cash balance sheet that puts it in the enviable position of having substantial financial wherewithal and flexibility, potentially enabling the company to identify value enhancing opportunities in a tumultuous environment. Fund management was able to build a position in BlueLinx at prices near tangible book value as housing sentiment continues to be depressed.

We see multiple paths for BlueLinx to return significant value to shareholders. In particular, the company has an opportunity to enhance operating margins closer to those of industry peers through internal initiatives that have been laid out and which seem attainable. The business is also one that embeds fixed cost leverage that can yield a dramatic amplification of return on invested capital during periods of higher distribution volumes or ones in which lumber prices are upward sloping.

Should BlueLinx successfully execute its growth initiatives, the company could garner the attention of numerous industry consolidators. The recently announced acquisition of Beacon Roofing by QXO is one example within the industry. There are also many private equity sponsors who are presently active in the industry improving the probabilities of a transaction and at a favorable price.

CONCLUSION

While no member of our portfolio management team has lived through a global trade war before, we have invested in uncertain and unfamiliar circumstances at a number of junctures throughout our careers. We do not recommend trying to time one’s entrances and exits from public markets, and certainly not in response to stock price volatility. Third Avenue’s historical success has stemmed from an embrace of stock price volatility while using the protections offered by cheap prices, strong balance sheets and a long-term investment horizon.

We thank you for your continued trust and support and look forward to writing to you again next quarter. In the interim, please don’t hesitate to contact us with any questions, comments, or ideas at clientservice@thirdave.com.

Sincerely,

The Third Avenue Small Cap Value Team

IMPORTANT INFORMATION

This publication does not constitute an offer or solicitation of any transaction in any securities. Any recommendation contained herein may not be suitable for all investors. Information contained in this publication has been obtained from sources we believe to be reliable, but cannot be guaranteed.

The information in this portfolio manager letter represents the opinions of the portfolio manager(s) and is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed are those of the portfolio manager(s) and may differ from those of other portfolio managers or of the firm as a whole. Also, please note that any discussion of the Fund’s holdings, the Fund’s performance, and the portfolio manager(s) views are as of March 31, 2025 (except as otherwise stated), and are subject to change without notice. Certain information contained in this letter constitutes “forward-looking statements,” which can be identified by the use of forward-looking terminology such as “may,” “will,” “should,” “expect,” “anticipate,” “project,” “estimate,” “intend,” “continue” or “believe,” or the negatives thereof (such as “may not,” “should not,” “are not expected to,” etc.) or other variations thereon or comparable terminology. Due to various risks and uncertainties, actual events or results or the actual performance of any fund may differ materially from those reflected or contemplated in any such forward-looking statement. Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Date of first use of portfolio manager commentary: April 19, 2025

1 The MSCI USA Small Cap Value Index captures small cap securities exhibiting overall value style characteristics across the US equity markets. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price and dividend yield. The index is not a security that can be purchased or sold.

2 The Russell 2000® Value Index measures the performance of small-cap value segment of the US equity universe. It includes those Russell 2000® companies with lower price-to-book ratios and lower forecasted growth values. The Russell 2000® Value Index is constructed to provide a comprehensive and unbiased barometer for the small-cap value segment. The index is completely reconstituted annually to ensure larger stocks do not distort the performance and characteristics of the true small-cap opportunity set and that the represented companies continue to reflect value characteristics. The index is not a security that can be purchased or sold.

For the Third Avenue Glossary please visit here.

Past performance is no guarantee of future results; returns include reinvestment of all distributions. The above represents past performance and current performance may be lower or higher than performance quoted above. Investment return and principal value fluctuate so that an investor’s shares, when redeemed, may be worth more or less than the original cost. For the most recent month-end performance please visit the Fund’s website at www.thirdave.com. The gross expense ratio for the Fund’s Institutional, Investor and Z share classes is 1.25%, 1.51% and 1.18%, respectively, as of March 1, 2025.

Risks that could negatively impact returns include: fluctuations in currencies versus the US dollar, political/social/economic instability in foreign countries where the Fund invests, lack of diversification, volatility associated with investing in small-cap securities, and adverse general market conditions.

The fund's investment objectives, risks, charges, and expenses must be considered carefully before investing. The prospectus contains this and other important information about the investment company, and it may be obtained by calling 800-443-1021 or visiting www.thirdave.com. Read it carefully before investing.

Distributor of Third Avenue Funds: Foreside Fund Services, LLC.

Current performance results may be lower or higher than performance numbers quoted in certain letters to shareholders.

Third Avenue offers multiple investment solutions with unique exposures and return profiles. Our core strategies are currently available through '40Act mutual funds and customized accounts. If you would like further information, please contact a Relationship Manager at:

Notice

You are now leaving the Third Avenue Management website and being connected to a third-party website. Please note that Third Avenue Management is not responsible for the information, content or products(s) found on third-party websites.